Singapore is one of the most important markets for crypto payment companies. That is why so many teams follow MAS, Singapore rules, and crypto compliance trends so closely. But this is also where many firms get the story wrong. They see an innovation-friendly market and assume speed is the main challenge. In practice, the harder challenge is control.

That is where MAS and crypto compliance connect. The Monetary Authority of Singapore does not judge firms only by product vision or market potential. It looks at whether they can manage risk once money starts moving. For payment teams, that means compliance is not just a legal step after launch. It is part of the system that makes growth possible.

Why MAS Matters

Singapore is a key market

Singapore matters because it is a trusted financial center with clear rules. That makes it attractive to exchanges, wallets, OTC desks, payment firms, and stablecoin businesses. Many teams want to grow in Singapore. Many others study Singapore because MAS often signals where crypto compliance standards may go next.

The core question is simple: what does MAS expect from firms that move crypto-linked value? The short answer is that MAS expects more than policy language. It expects real control.

MAS shapes trust

MAS does more than approve licences. It shapes the trust standard for the market. It affects how firms onboard users, monitor transactions, handle incidents, and explain risk to banks, partners, and regulators.

This matters because payment companies are not judged only by product quality. They are judged by control quality too. A firm can offer smooth payments and still create serious risk if its compliance and monitoring systems are weak.

In Singapore, trust is operational. MAS expects firms to build trust into flows, controls, and decisions.

MAS is not anti-crypto

It is easy to describe MAS as either crypto-friendly or strict. Neither label says enough. MAS is better understood as open to innovation, but unwilling to accept weak controls.

That distinction matters. MAS is not trying to stop crypto payment activity. It is trying to stop firms from moving value without being able to explain risk. From a BlockSec view, that is the right way to understand crypto compliance in Singapore.

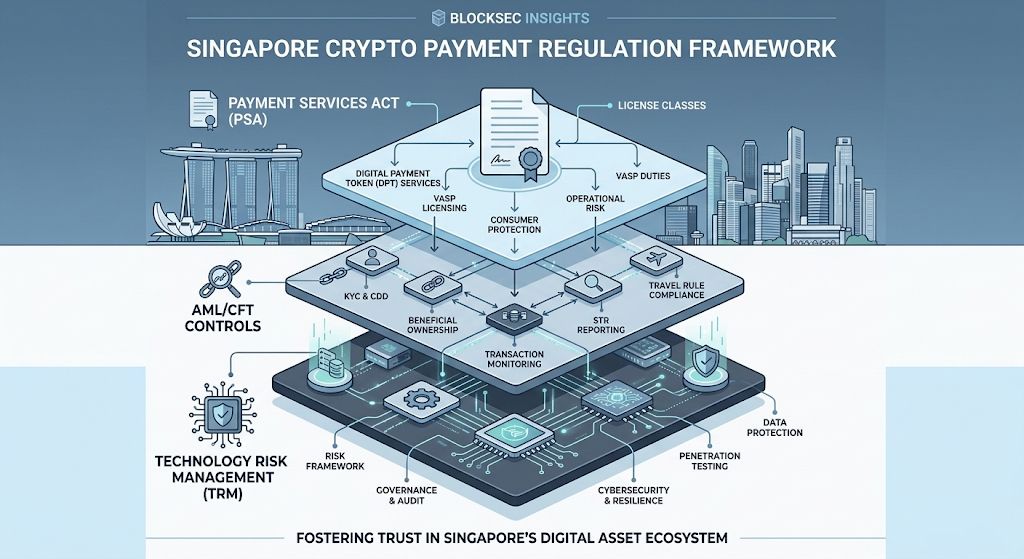

What MAS Regulates

The PSA sets the base

For payment companies, the Payment Services Act is the starting point. It is the main framework that tells firms whether their activity falls inside regulated payment services. It also matters for services tied to Digital Payment Token, or DPT, activity.

MAS focuses on real activity, not marketing language. A team may describe itself as a payment platform, settlement layer, or merchant tool. But if the service touches DPT activity in the wrong way, the compliance burden changes.

As of March 12, 2026, MAS’ showed 37 entries, and all 37 were listed as Major Payment Institutions. That tells us MAS does not treat this area as a light-touch category.

Legal does not mean light-touch

Crypto payment activity in Singapore can be lawful. But lawful does not mean loose. MAS also makes clear in its Currency FAQs that notes and coins issued by MAS are legal tender in Singapore. Crypto does not hold that same status, even though regulated crypto-related payment services can still operate lawfully.

This helps explain MAS’ approach. The regulator is not giving payment firms a blank check. It is saying that if they want to move value in Singapore, they need a strong compliance framework around that activity.

Technology risk matters too

Many teams think crypto compliance is mostly about AML/CFT. That view is too narrow. MAS also cares about technology risk and system resilience. MAS has published Technology Risk Management FAQs that explicitly cover payment services licence holders carrying on digital payment token service.

This is where many firms miss the deeper point. In crypto payments, compliance and security are not separate lanes. A weak monitoring system is a compliance problem. A delayed incident response can become a regulatory problem. A poor transaction review flow can become both.

Why Payment Firms Feel Pressure

Payments expose weak controls

Payment businesses feel MAS pressure early because payments expose weak controls faster than many other crypto products do. Funds move quickly. Value crosses accounts, chains, and counterparties. Merchant flows settle on tight timelines. Cross-border paths add more complexity.

That means mistakes do not stay abstract. They show up in live operations. A weak review process becomes user friction. A missed risk signal becomes exposure. A slow escalation path becomes a real business problem.

This is why firms often discover that compliance is not just a legal issue. It is also a speed issue, a trust issue, and an operating issue.

KYC is only the start

A lot of firms still build compliance around onboarding. They focus on KYC, then assume the core job is done. For crypto payments, that logic fails too early.

KYC helps answer who the customer is. It does not answer where the assets came from, what path they took, or whether the funds are linked to a hack, a scam cluster, sanctions exposure, or another source of risk. In payment flows, those questions matter every day.

That is why the real compliance model in Singapore has moved beyond onboarding. MAS expects firms to build live risk controls around asset flows, not just identity checks at the door.

Onchain risk keeps changing

Onchain risk is not static. Addresses change. Risk clusters evolve. Funds are bridged, split, parked, and re-entered. A wallet that looked normal last month may not look normal now.

For payment companies, this means delayed review is often weak review. If a team can only understand a risky flow hours later, the platform may already hold the exposure. In a market where MAS expects firms to prove control, that delay matters.

What MAS Expects

Firms must know their status

The first expectation is simple. Firms need to know what activity they are really performing in Singapore. Not what the internal team calls it. Not what the marketing page says. The real product flow matters.

This sounds obvious, but it is where many problems begin. Payment companies often evolve quickly. A product starts as one type of service, then adds custody features, merchant settlement, wallet flows, or cross-border functions. If the compliance model does not evolve with the product, risk builds quietly.

Firms must know their customer

Customer due diligence still matters. MAS expects firms to understand who the customer is, what relationship the firm has with that customer, and where enhanced review is needed.

But this is only the first layer. In crypto payments, a clean onboarding file does not guarantee a clean transaction flow. A payment company needs to keep looking after the customer is live.

Firms must monitor transactions

This is where many teams either mature or stall. Monitoring has to continue after onboarding. A firm needs to watch for suspicious behavior, unusual fund paths, risky counterparties, and changes in transaction patterns.

That sounds simple, but it is hard in practice. Crypto transactions do not behave like bank wires. Funds can move across wallets, chains, bridges, and contracts in ways that make manual review too slow and too narrow.

From a BlockSec view, this is the real pressure point. Firms do not struggle because MAS rules are impossible to read. They struggle because turning MAS expectations into live controls is operationally hard.

Firms must keep records

MAS-style compliance also depends on recordkeeping and clear decisions. If a transaction is allowed, delayed, escalated, or blocked, the firm should be able to explain why. That means keeping a clean trail of alerts, reviews, decisions, and outcomes.

This is not only about satisfying MAS later. It also helps with internal accountability, partner due diligence, banking relationships, and post-incident analysis. A control system without memory is not a strong control system.

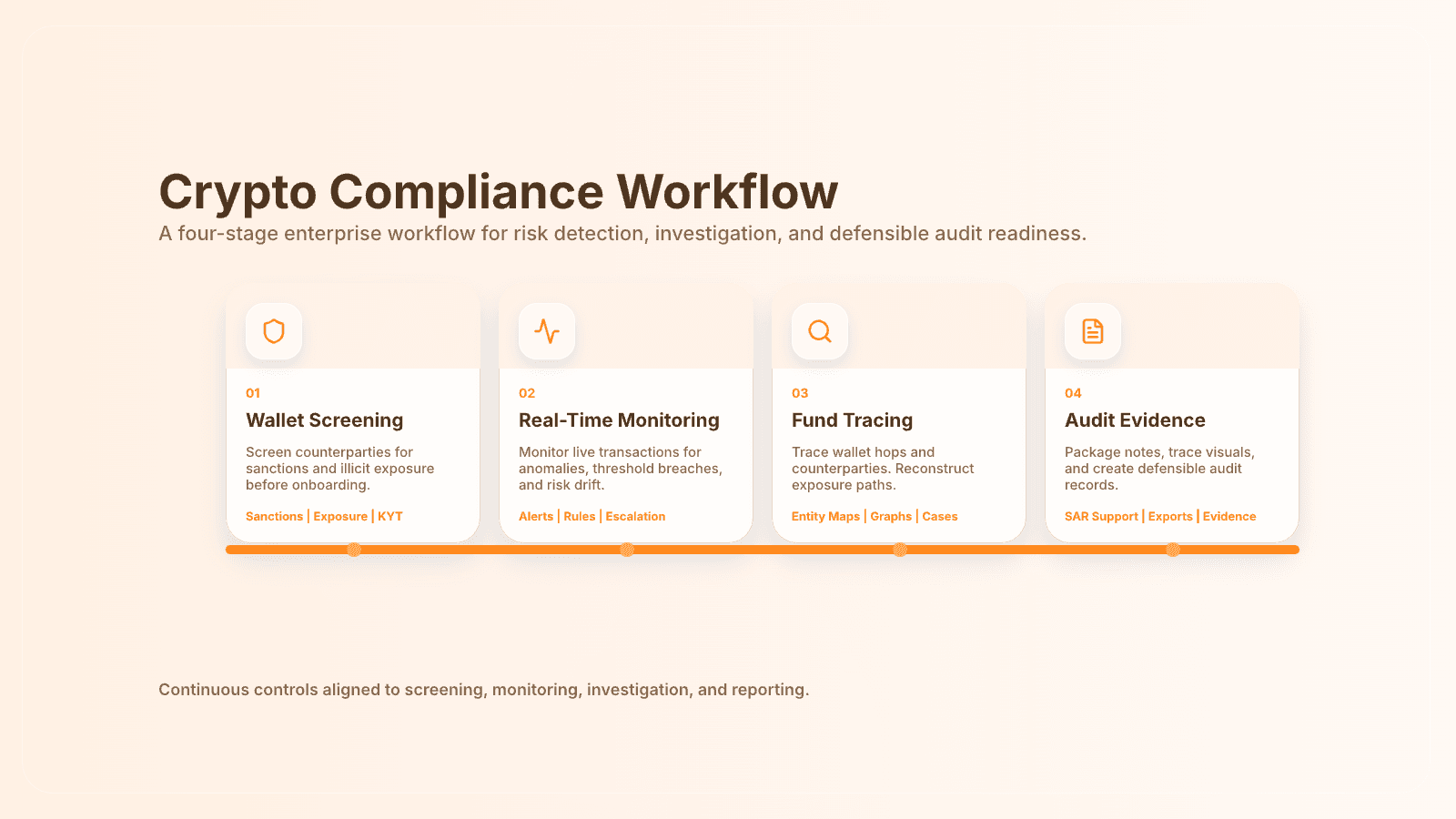

How Strong Controls Work

Screening moves the line earlier

A strong compliance stack starts before loss. Wallet screening helps firms understand whether a counterparty carries sanctions risk, illicit exposure, or other warning signs before value enters the platform.

This matters because payment systems are much harder to clean up after risky funds are already inside. The earlier the control point, the more useful the control becomes.

BlockSec’s Crypto Payment Solutions page lays out this shift clearly: payment firms need real-time KYA/KYT, dynamic controls, and evidence-ready workflows, not just static checks.

Monitoring keeps the system live

The second layer is real-time transaction monitoring. Screening once is not enough because risk changes over time. A user’s counterparties may change. The source of funds may change. The route of the asset may change.

A payment company that only checks risk at onboarding is not really managing a live system. It is managing a snapshot.

This is exactly the problem BlockSec addresses in Phalcon Compliance, where screening, live monitoring, case management, and reporting are built into one workflow.

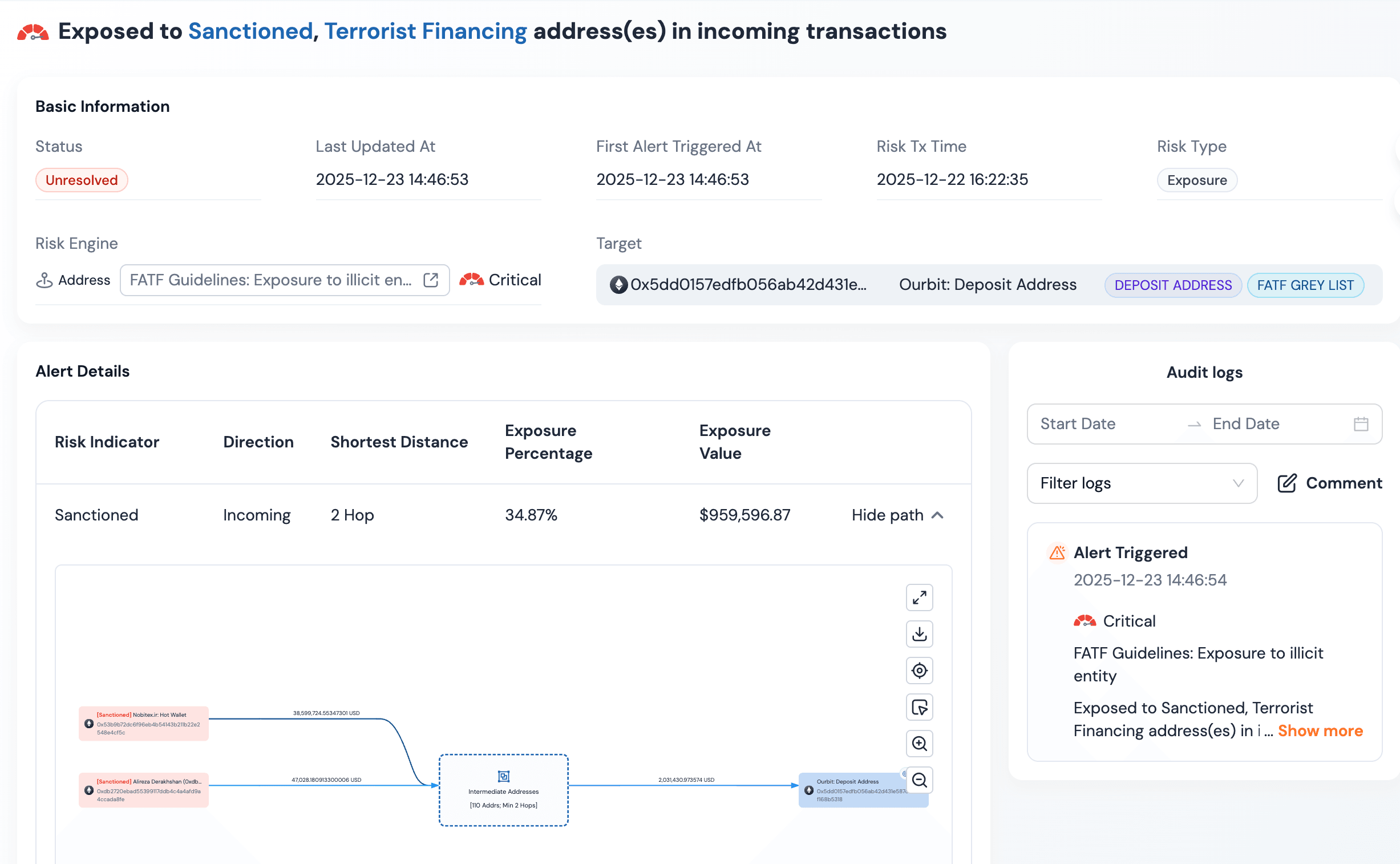

Tracing explains difficult cases

When a transaction is flagged, the team needs more than a score. It needs context. Where did the funds come from? What clusters did they touch? Was the flow normal, or did it follow a suspicious route?

That is where tracing becomes important. Alerts tell the team there may be a problem. Tracing helps explain the problem. For payment companies, this is often the difference between noise and defensible action.

BlockSec’s article, Crypto Exchange Compliance with Emphasis on Real-Time AML/CFT Control in 2026, makes the same point from an exchange angle: KYC and basic AML are not enough when risk sits in the fund flow itself.

Evidence protects the business

The last layer is evidence. Good firms keep records of alert logic, review notes, escalation decisions, and outcomes. This helps during audits, partner reviews, and real investigations. It also helps teams improve their controls over time.

In other words, compliance does not only need detection. It also needs explanation.

What This Means for the Industry

Compliance is now infrastructure

For payment companies in Singapore, crypto compliance is no longer a thin legal wrapper around the business. It is part of the business itself. It shapes whether a firm can scale with partners, support merchants, keep banking access, and handle scrutiny without losing momentum.

That is why the best operators no longer ask how little compliance they can get away with. They ask what kind of control system lets them grow without breaking trust.

MAS is raising the bar

Seen clearly, MAS is doing something important for the market. The Monetary Authority of Singapore is raising the bar for what a serious payment company looks like. Not a company with polished messaging, but a company that can explain flows, manage risk, respond to incidents, and support real oversight.

That is a healthy direction for the sector. As crypto payments become more useful, the cost of weak controls goes up. The firms that survive in Singapore will be the ones that can move fast without losing discipline.

Trust decides who lasts

This is the clearest takeaway. MAS and crypto compliance are tightly linked because MAS is effectively defining what trusted crypto payment infrastructure should look like in Singapore.

For payment teams, the lesson is simple. MAS is not asking firms to be perfect. It is asking them to be defensible. In practice, that means screening wallets, monitoring transactions, tracing risky flows, and documenting decisions while the business is still moving.

That is also where strong compliance becomes a growth advantage. It supports trust, and in payments, trust decides who lasts.