Kürzlich kündigte der australische Minister für Inneres, Tony Burke, offiziell neue Vorschriften an, die sich gegen Krypto-Geldautomaten richten und diese als „Produkte mit hohem Risiko“ einstufen, die mit Geldwäsche, Betrug und Kindesausbeutung in Verbindung gebracht werden.

Laut Burke ist die Zahl der Krypto-Geldautomaten in Australien innerhalb von sechs Jahren von nur 23 auf über 2.000 gestiegen. Eine Untersuchung der AUSTRAC ergab, dass 85 % der großen Transaktionen, die über diese Terminals abgewickelt wurden, mit Betrügereien oder illegalen Aktivitäten verbunden waren.

Die vorgeschlagene Gesetzgebung würde die AUSTRAC ermächtigen, Produkte mit hohem Risiko einzuschränken oder zu verbieten, einschließlich Krypto-Geldautomaten. Burke bestätigte, dass der Gesetzentwurf in den kommenden Monaten dem Parlament vorgelegt wird.

Unterdessen gab das US-amerikanische Financial Crimes Enforcement Network (FinCEN) am 4. August 2025 die Mitteilung FIN-2025-NTC1 heraus, in der es Finanzinstitute vor illegalen Aktivitäten im Zusammenhang mit Convertible Virtual Currency (CVC) Kiosken – dem technischen Begriff für Krypto-Geldautomaten – warnte und klare Erwartungen für Suspicious Activity Reports (SARs) und die Einhaltung von AML-Verpflichtungen festlegte.

Unterdessen gab das US-amerikanische Financial Crimes Enforcement Network (FinCEN) am 4. August 2025 die Mitteilung FIN-2025-NTC1 heraus, in der es Finanzinstitute vor illegalen Aktivitäten im Zusammenhang mit Convertible Virtual Currency (CVC) Kiosken – dem technischen Begriff für Krypto-Geldautomaten – warnte und klare Erwartungen für Suspicious Activity Reports (SARs) und die Einhaltung von AML-Verpflichtungen festlegte.

Verständnis von CVC-Kiosken und deren Ausnutzung bei Finanzkriminalität

CVC-Kioske funktionieren ähnlich wie herkömmliche Geldautomaten, indem sie es Benutzern ermöglichen, mit Bargeld Kryptowährungen zu kaufen oder zu verkaufen. Sie sind häufig in Convenience Stores, Tankstellen und Einkaufszentren zu finden und unterstützen in der Regel Bitcoin-Transaktionen sowie andere Kryptowährungen wie Litecoin und Ethereum.

Dennoch sind ihre Risiken immer offensichtlicher geworden und machen sie zu Hauptzielen für Finanzkriminalität und illegale Aktivitäten. Die Anonymität und Geschwindigkeit von Transaktionen über Krypto-Geldautomaten stellen erhebliche Herausforderungen für die Blockchain-Sicherheit dar.

Dennoch sind ihre Risiken immer offensichtlicher geworden und machen sie zu Hauptzielen für Finanzkriminalität und illegale Aktivitäten. Die Anonymität und Geschwindigkeit von Transaktionen über Krypto-Geldautomaten stellen erhebliche Herausforderungen für die Blockchain-Sicherheit dar.

Im Jahr 2024 erhielt das Internet Crime Complaint Center (IC3) des FBI über 10.900 Beschwerden im Zusammenhang mit Betrug an Krypto-Geldautomaten, wobei die Verluste der Opfer über 246,7 Millionen US-Dollar betrugen – ein Anstieg der Fälle um 99 % und der Verluste um 31 % im Vergleich zu 2023.

Die FTC berichtete ebenfalls über einen „explosionsartigen Anstieg“ von Betrügereien mit Krypto-Geldautomaten.

Die Gründe liegen auf der Hand: Sobald eine Krypto-Überweisung ausgeführt ist, ist sie nahezu unumkehrbar und augenblicklich, im Gegensatz zu herkömmlichen Banküberweisungen, deren Abwicklung Tage dauern kann. Dies gibt den Opfern praktisch keine Zeit, verlorene Gelder zurückzufordern. Dieses Merkmal, das für legitime Zwecke attraktiv ist, ist ein wichtiger Wegbereiter für Betrug und Geldwäsche.

Alarmierenderweise sind Senioren die Hauptopfer – Personen ab 60 Jahren fallen dreimal häufiger Krypto-Geldautomat-Betrügereien zum Opfer und machen zwei Drittel aller gemeldeten Verluste aus. Diese demografische Gruppe ist oft weniger vertraut mit den Nuancen der Blockchain-Sicherheit und der Unumkehrbarkeit von Krypto-Transaktionen.

Krypto-Geldautomaten als Werkzeuge für Geldwäsche und organisierte Kriminalität

Über Betrügereien hinaus sind CVC-Kioske zu mächtigen Werkzeugen für Drogenkartelle und organisierte Kriminalität geworden. Ihre Fähigkeit, anonyme und schnelle Transaktionen zu ermöglichen, macht sie ideal für Geldwäsche.

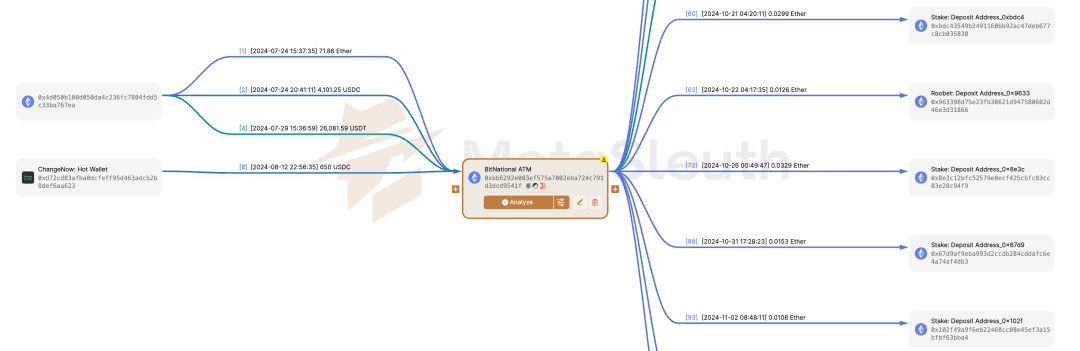

FinCENs Analyse von Daten des Bank Secrecy Act (BSA) zeigt die häufige Nutzung von Kiosken zur Reinigung von Drogengewinnen. Die US Drug Enforcement Administration (DEA) bestätigte ferner, dass transnationale kriminelle Gruppen wie das Jalisco New Generation Cartel (CJNG) zunehmend auf CVC für schnelle grenzüberschreitende Überweisungen angewiesen sind, die die Risiken des traditionellen Bargeldschmuggels umgehen. Dies verdeutlicht eine kritische Lücke in der AML-Durchsetzung.

In Illinois gibt es beispielsweise 1.626 Krypto-Geldautomaten, davon über 1.100 allein in Chicago – einem wichtigen Knotenpunkt für die Geldwäsche von Kartellgeldern.

DEA-Untersuchungen ergaben, dass Kriminelle aus anderen Bundesstaaten sogar nach Chicago reisen, um Drogengelder in Krypto umzuwandeln, bevor sie sie ins Ausland schicken. Dieses Muster unterstreicht die globale Natur der Finanzkriminalität und die Herausforderungen bei der Regulierung dieser dezentralen Werkzeuge.

Die Compliance-Landschaft für CVC-Betreiber

Weltweit ist die Zahl der Krypto-Geldautomaten sprunghaft angestiegen – allein in den USA von 4.128 auf 37.342 Maschinen in sechs Jahren, während Hongkong SAR rund 224 Einheiten eingesetzt hat, die sich meist in belebten Geschäftsvierteln wie Mong Kok konzentrieren.

FinCEN warnt jedoch, dass die Compliance-Rate unter den CVC-Betreibern „alarmierend niedrig“ ist. Viele operieren unter Verstoß gegen die BSA-Verpflichtungen, was die Risiken für Finanzkriminalität dramatisch erhöht und die Blockchain-Sicherheit untergräbt.

Was legitime Betreiber für die AML-Compliance tun müssen

Nach dem BSA gelten Betreiber von CVC-Kiosken als Money Services Businesses (MSBs) – das bedeutet, dass der Betrieb ohne Registrierung einer Bankentätigkeit ohne Lizenz gleichkommt. Verstöße werden strafrechtlich verfolgt. Dies ist ein Eckpfeiler der AML-Vorschriften.

Sie müssen:

- Sich innerhalb von 180 Tagen nach Betriebsaufnahme bei FinCEN registrieren.

- Große oder verdächtige Transaktionen melden – Currency Transaction Reports (CTR) für Bargeldtransaktionen über 10.000 US-Dollar und Suspicious Activity Reports (SARs) für verdächtige Aktivitäten über 2.000 US-Dollar einreichen.

- Kundenidentifikations- und Transaktionsdaten für mindestens 5 Jahre aufbewahren. Dazu gehören robuste KYC (Know Your Customer)-Verfahren.

Bundesstaaten wie Kalifornien gehen weiter und begrenzen tägliche Transaktionslimits pro Kunde auf 1.000 US-Dollar. In Iowa verklagte der Generalstaatsanwalt zwei Betreiber, deren Kioske über 20 Millionen US-Dollar an Betrug ermöglichten. Diese Maßnahmen zielen darauf ab, die Blockchain-Sicherheit zu verbessern und Geldwäsche zu verhindern.

Benötigen Sie robuste AML-Lösungen für Ihr Web3-Projekt?

BlockSec bietet fortschrittliche On-Chain-Überwachungs- und Compliance-Tools zur Erkennung und Verhinderung illegaler Aktivitäten. Schützen Sie Ihre Benutzer und stellen Sie die Einhaltung von Vorschriften sicher.

Weitreichende Verstöße und Durchsetzungsmaßnahmen gegen Krypto-Geldautomaten-Betreiber

Eine Untersuchung in New Jersey aus dem Jahr 2021 ergab, dass ein Drittel der Betreiber nicht bei FinCEN registriert war. Andere ignorierten KYC-Anforderungen und akzeptierten Transaktionen allein auf der Grundlage von Telefonnummern oder E-Mail-Adressen – ideale Bedingungen für Betrüger und Geldwäsche.

Einige falsifizierten sogar Geschäftsanmeldungen, nutzten persönliche oder gefälschte Firmenbankkonten und strukturierten Transaktionen, um die CTR/SAR-Schwellenwerte zu umgehen, eine Praxis, die nach Bundesrecht streng verboten ist. Diese Handlungen untergraben direkt die AML-Bemühungen und setzen Benutzer erheblichen Betrugsrisiken aus.

FinCENs Mitteilung nennt konkrete Durchsetzungsbeispiele:

FinCENs Mitteilung nennt konkrete Durchsetzungsbeispiele:

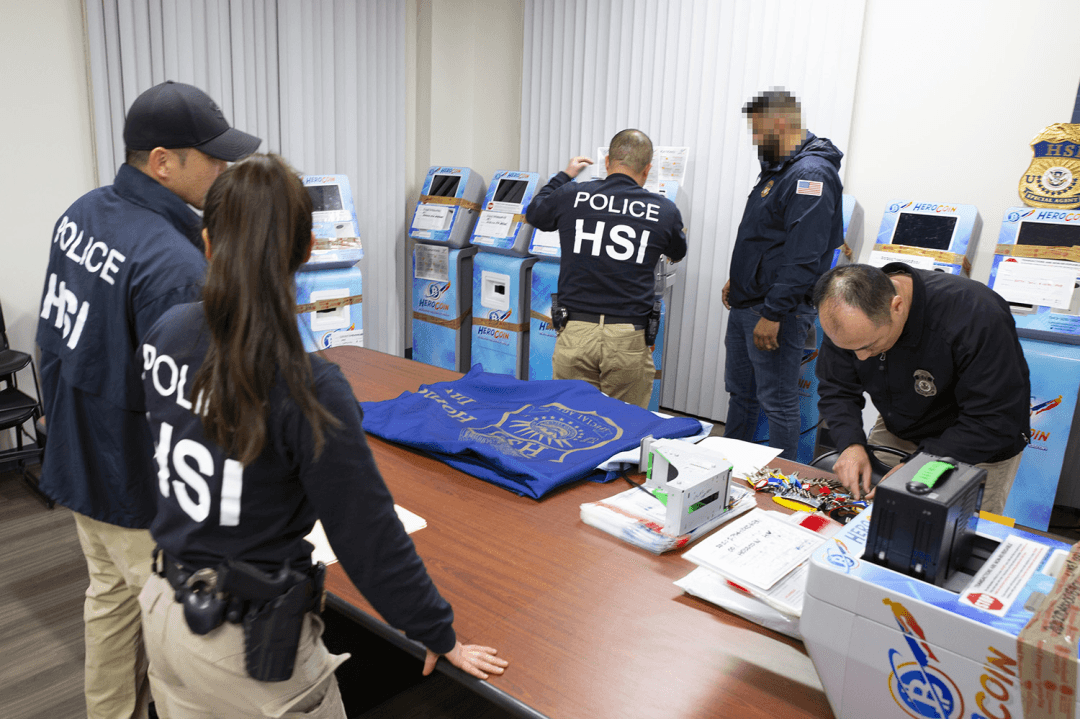

- Orange County Fall (2021): Der ehemalige Bankangestellte Kais Mohammad betrieb ein nicht registriertes Geldautomaten-Netzwerk, das über 25 Millionen US-Dollar abwickelte, keine AML-Prüfungen implementierte und zu 24 Monaten Haft verurteilt wurde. Dieser Fall unterstreicht die schwerwiegenden Folgen der Vernachlässigung von Compliance- und Blockchain-Sicherheits-Protokollen.

- New Hampshire Fall (2022): Drei Betreiber nutzten gefälschte Firmenkonten für Bar-Einzahlungen an Krypto-Geldautomaten und wurden wegen Drahtbetrugs verurteilt, mit Haft und Geldstrafen.

Dutzende ähnliche Strafverfolgungen haben landesweit stattgefunden, mit Geldstrafen in Millionenhöhe und obligatorischer Einziehung illegaler Erträge. Diese Durchsetzungsmaßnahmen dienen als eindringliche Warnung an alle Betreiber im Bereich digitaler Vermögenswerte hinsichtlich der Bedeutung robuster AML- und Compliance-Frameworks.

Lektionen für die Web3-Industrie: Priorisierung von Compliance und Blockchain-Sicherheit

Während die Maßnahmen von FinCEN und AUSTRAC auf physische Krypto-Geldautomaten abzielen, spiegeln sie eine breitere Botschaft für das gesamte Web3-Ökosystem wider: Compliance ist nicht optional – sie ist existenziell. Von Betrügern, die AML-Lücken ausnutzen, bis hin zu Betreibern, die strafrechtlich verfolgt werden, unterstreichen diese Fälle eine Wahrheit: „Risiko kennt keine Grenzen und Compliance keine Abkürzungen.“ Dieses Prinzip ist für die Gewährleistung der Blockchain-Sicherheit von größter Bedeutung.

Die Lektion geht über Krypto-Geldautomaten hinaus – sie gilt für Börsen, DeFi-Protokolle und Zahlungsplattformen. Da globale Regulierungsbehörden von einer reaktiven zu einer proaktiven Durchsetzung übergehen, werden integrierte AML-Tools und On-Chain-Monitoring-Lösungen, wie sie von BlockSec angeboten werden, zu essentieller Infrastruktur für das digitale Finanzwesen. Diese Werkzeuge sind entscheidend für die Erkennung und Verhinderung von Finanzkriminalität und illegalen Aktivitäten.

Web3-Innovation sollte niemals auf Kosten von Compliance und Blockchain-Sicherheit gehen – und dieser globale Schlag beweist es. Proaktive Maßnahmen, einschließlich gründlicher Smart-Contract-Audits und kontinuierlicher On-Chain-Überwachung, sind für jedes Projekt unerlässlich, das auf langfristige Nachhaltigkeit und Vertrauen im Bereich digitaler Vermögenswerte abzielt.