For exchanges, payment gateways, banks, and card issuers, the importance of Web3 Compliance cannot be overstated. Regulators demand AML controls, sanctions screening, and cross-border monitoring. Without a clear Web3 Compliance framework, institutional partnerships stall and market access becomes fragile.

Have you ever burnt out by following scenarios? Missing high-risk address, unmonitoring transaction, reporting delay...... All of these may lead to regulatory scrutiny, frozen accounts, blocked banking channels, and reputational damage. For payment leaders and licensed exchanges, knowing what Web3 Compliance needs can one of the most pivotal factors to facilitate your financial activities.

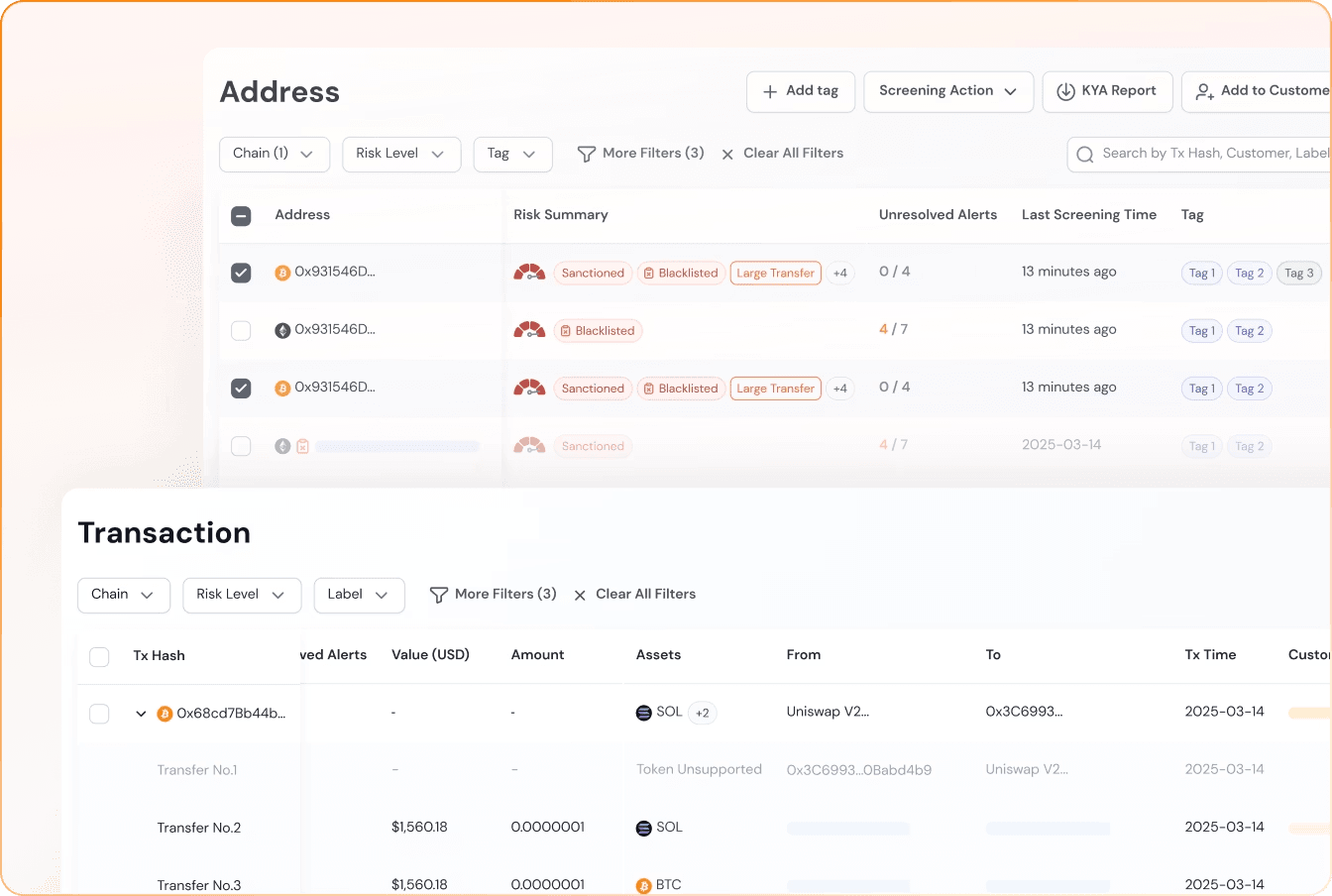

That's where Phalcon Compliance comes in, giving you a powerful real-time Web3 toolkit built for institutions. With address screening, transaction monitoring, customizable AML engines, one-click STR/SAR exports, and fund tracing via MetaSleuth, you can stay compliant across markets. It also empowers you to detect risk early, automate controls at scale, and move forward with confidence. Simultaneously, regulators, partners, and banks see a framework they trust.

What Web3 Compliance Is

Web3 Compliance refers to the structured framework of controls designed to manage regulatory, financial crime, and operational risks within decentralized blockchain ecosystems. As Web3 shifts internet architecture from centralized platforms to decentralized networks, traditional compliance expectations do not disappear. Instead, they evolve. Regulators still expect accountability, transparency, and protection against illicit activity, even in permissionless environments.

At its foundation, Web3 is built on decentralization, cryptography, peer-to-peer interaction, and smart contracts. These features enhance transparency and reduce centralized control. However, they also introduce new forms of risk. Pseudonymous identities, irreversible transactions, tokenized assets, and cross-border fund movement can create exposure to money laundering, sanctions violations, fraud, and financial manipulation.

Web3 Compliance therefore extends beyond technical security. While smart contract audits, wallet protection, and infrastructure safeguards address code-level vulnerabilities, compliance focuses on financial behavior and regulatory responsibility. It ensures that platforms can identify high-risk actors, monitor suspicious transactions, manage cross-chain exposure, and maintain defensible reporting processes.

Another defining element of Web3 Compliance is accountability in a decentralized environment. With limited centralized supervision, platforms must embed monitoring, risk controls, and documentation directly into their operational systems. This includes screening mechanisms, transaction analysis, structured reporting workflows, and audit trails that demonstrate adherence to AML and CFT obligations.

Why AML and CFT Are Primary Focus of Web3 Compliance

Before we talk about tools, alerts, or reporting, we need to be clear about one thing. What is Web3 Compliance? Web3 Compliance is not about smart contract security and infrastructure uptime. At its core, Web3 Compliance is an AML and CFT control framework built for blockchain-based financial systems.

In Web2 finance, compliance means KYC, transaction monitoring, sanctions screening, and suspicious activity reporting. In Web3, the environment changes, but the regulatory expectation does not. Regulators still care about illicit funds, terrorism financing, sanctions exposure, and cross-border money movement.

That is why AML and CFT sit at the center of Web3 Compliance. If you cannot screen wallets, monitor transactions, detect suspicious activity, and produce formal reports, you are not compliant, no matter how decentralized your technology is.

This point is also proven by global regulatory expectations. International bodies such as the Financial Action Task Force (FATF) have made it clear that virtual asset service providers must follow AML and CFT obligations similar to traditional financial institutions.

This includes sanctions screening, transaction monitoring, suspicious activity reporting, and compliance with cross-border requirements. Regulators across the United States, Europe, Hong Kong, and Singapore are increasing enforcement actions against platforms that fail to control illicit fund flows.

As digital assets become more integrated into mainstream finance, regulators expect the same level of transparency and accountability that applies to banks and payment institutions. Web3 Compliance is therefore not optional. It is a structural requirement for operating legally and maintaining institutional trust.

Risk and Anonymity Exposure

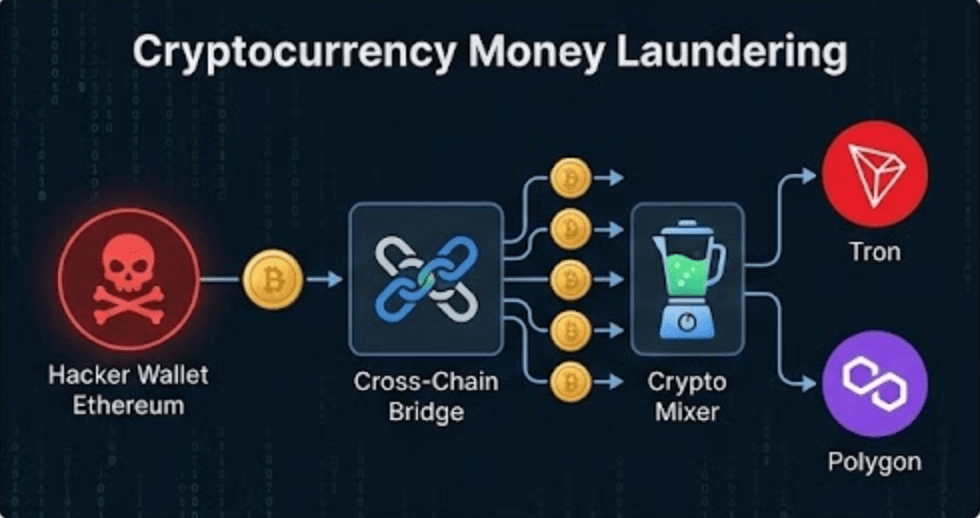

Web3 allows users to stay pseudonymous. That creates freedom, but it comes along with compliance risk. Regulators worry about terrorism financing, sanctions evasion, and illegal money flows. Web3 Compliance requires strong address screening and high-risk wallet identification. You need to know whether a wallet is linked to sanctioned entities, mixers, darknet markets, or exploit funds.

Fund Flows Instead of Only Code

Web3 Compliance focuses on financial behavior. Even if your code is secure, illicit funds can still move through your platform. You must monitor transactions continuously. Abnormal fund flows, rapid transfers between wallets, and cross-chain exposure are red flags.

Structured Reporting

One major gap in many Web3 projects is proof. You may claim to monitor activity, but can you demonstrate it? Regulators expect documentation, not promises. Web3 Compliance means having structured review records, risk handling documentation, and formal reporting workflows.

Adaptation to Different Regulatory Environments

Web3 operates globally, but compliance rules differ by region. What is acceptable in one jurisdiction may trigger enforcement in another. Web3 Compliance requires flexible risk engines. You must adjust thresholds, scoring logic, and monitoring rules based on local AML and sanctions expectations.

How to Meet Web3 Compliance’s Requirements

The biggest shift in Web3 Compliance is this: it cannot live in a policy document. It must live inside your system. Screening, monitoring, alerting, reporting, and fund tracing must operate together as a single compliance infrastructure. Compliance is no longer paperwork. It is embedded control.

Web3 Compliance usually begins before funds even move. The moment a wallet interacts with your platform, risk exposure begins. That is why real-time address screening becomes the first operational layer of AML and CFT enforcement. It turns regulatory expectations into daily execution.

Before accepting deposits, you need to assess the source address immediately. If a wallet is linked to sanctions, exploits, mixers, or other high-risk entities, you must detect it at entry. Early detection prevents contaminated liquidity, protects banking relationships, and reduces downstream investigation costs.

Withdrawal controls are equally critical. Outgoing transfers represent regulatory liability. Real-time screening of destination wallets ensures you do not facilitate sanctioned activity or illicit fund movement. Blocking or reviewing risky withdrawals protects licenses, payment rails, and institutional partnerships.

Sanctions list matching should not rely on manual checks. In a scalable Web3 Compliance framework, screening must run continuously against updated risk databases. Automated matching ensures that evolving sanctions lists and global watchlists are reflected instantly in operational decisions.

High-risk entity identification must go beyond a simple flag. Compliance teams need context. Why is this address risky? Is it linked to terrorism financing, ransomware, darknet markets, or layered laundering activity? Structured risk intelligence allows faster case handling and more defensible reporting.

This is where infrastructure matters. To address this, Phalcon Compliance operationalizes these controls in real time, but the core principle remains the same: Web3 Compliance only works when AML and CFT logic are embedded directly into transaction flows, not reviewed after exposure occurs.

Strengthen Web3 Compliance with Real-Time Transaction Monitoring

Web3 Compliance cannot rely on entry-point controls alone. Risk does not only appear at deposit or withdrawal. It can emerge during transaction activity, as funds move, split, or interact with other wallets. Continuous monitoring is what keeps compliance active after onboarding.

On-chain behavior changes fast. A wallet that looked normal at first can suddenly engage in unusual patterns. Large value spikes, unexpected routing paths, or interactions with high-risk clusters may signal emerging threats. Real-time transaction monitoring allows you to detect these signals while activity is still unfolding.

Velocity is a major compliance indicator. Rapid transfers across multiple wallets within short time windows can suggest layering or concealment strategies. A strong Web3 Compliance framework must identify these behaviors early, before risk spreads across internal accounts or customer balances.

Cross-chain movement adds another layer of complexity. Funds can bridge between networks in minutes, creating fragmented exposure. Web3 Compliance requires visibility across chains to understand whether suspicious activity is isolated or part of a broader laundering path.

Detection alone is not enough. Signals must convert into action. Structured alerts, review queues, and escalation workflows transform monitoring data into operational control. Compliance teams need clear case prioritization, documented review steps, and consistent decision logic.

A high-performance toolkit like Phalcon Compliance operationalizes this layer of Web3 Compliance by combining behavioral analysis, real-time alerts, and structured workflows. But the principle remains simple: monitoring must be continuous, contextual, and integrated into daily transaction flow.

Scale Web3 Compliance Across Different Regulatory Environments

Web3 Compliance does not operate in a single regulatory vacuum. Every jurisdiction applies its own AML and CFT standards, sanctions scope, and reporting expectations. If you serve users across regions, your compliance framework must adapt without losing structural consistency.

A rigid rule set cannot support global operations. Thresholds that are acceptable in one market may be insufficient in another. Web3 Compliance requires configurable risk logic, so monitoring intensity and escalation triggers can reflect local regulatory requirements.

Risk assessment should also be dynamic. Some markets prioritize sanctions exposure. Others focus heavily on transaction velocity or cross-border flows. A flexible compliance engine allows you to adjust scoring weight, behavioral indicators, and review criteria according to your operating model.

Automation is essential for scale. Once regulatory logic is configured, alerts, prioritization, and workflow routing should operate automatically. This reduces dependence on manual interpretation and ensures consistency across compliance teams in different regions.

A system such as Phalcon Compliance enables this level of configurability, but the broader principle remains clear: Web3 Compliance must function as a regulatory framework that can evolve with jurisdictions, not a static checklist tied to one market.

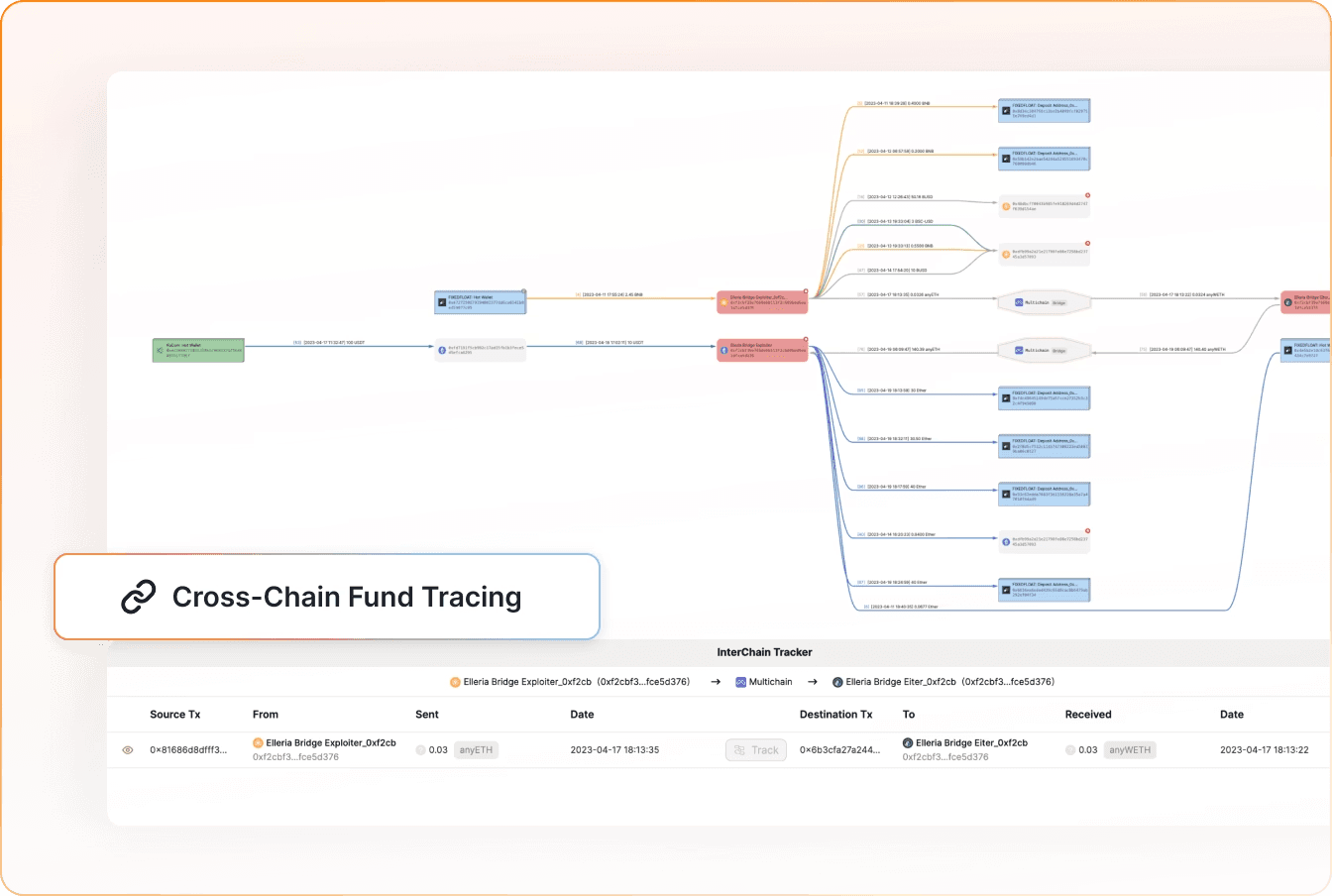

Deepen Web3 Compliance Through Structured Fund Tracing

Web3 Compliance does not stop at detection. When alerts are triggered, compliance teams must investigate, validate, and document findings. Basic monitoring signals are only the starting point. Complex cases require deeper transaction analysis.

Illicit funds rarely move in straight lines. They are split, routed, layered, and bridged across multiple wallets. A strong Web3 Compliance framework must support fund path reconstruction. You need to trace how assets traveled, where exposure originated, and which entities are connected.

Clear fund flow visibility strengthens regulatory defensibility. When you can demonstrate the source of funds, identify high-risk clusters, and map transaction chains, your investigation becomes evidence-based. This reduces uncertainty and improves the quality of STR and SAR reporting.

For centralized exchanges and payment platforms, tracing is especially critical. Deposit origin validation, suspicious withdrawal analysis, and linked wallet identification require structured analytical tools. Compliance decisions must rely on traceable data, not assumptions.

A solution such as Phalcon Compliance integrates fund tracing through MetaSleuth to support this investigative layer. But at its core, Web3 Compliance requires the ability to move from signal detection to structured case investigation with clarity and confidence.

Applications of Web3 Compliance Across Different Scenarios

Apply Web3 Compliance in Crypto Payment Platforms

Crypto payment platforms operate under constant transaction pressure. Deposits arrive from unknown wallets across multiple jurisdictions. Withdrawals move funds globally within minutes. In this environment, Web3 Compliance must function as a live control system, not a periodic review process.

Inbound transactions carry immediate exposure. A single high-risk deposit linked to sanctions, ransomware, or fraud can contaminate liquidity and trigger banking concerns. Web3 Compliance requires instant risk evaluation at the point of entry, ensuring suspicious funds are identified before settlement risk increases.

Outbound transfers create regulatory liability. If assets are sent to sanctioned or illicit destinations, the responsibility does not disappear because the transaction is on-chain. Real-time withdrawal controls are essential to prevent regulatory violations and protect payment licenses.

Operational efficiency is equally important. Payment providers cannot rely on manual compliance reviews while handling high transaction volumes. Structured alerts, automated case routing, and standardized reporting workflows allow compliance teams to act quickly without slowing down business flow.

Strong Web3 Compliance transforms payment infrastructure into a controlled financial environment. It balances speed with regulatory discipline, enabling platforms to scale while maintaining trust with banks and regulators.

A system such as Phalcon Compliance supports this framework by embedding screening, monitoring, and reporting directly into payment operations, turning AML and CFT requirements into automated daily execution.

Strengthen Web3 Compliance in Centralized Exchanges

Centralized exchanges operate in one of the most complex compliance environments in Web3. Deposits, internal transfers, margin activity, derivatives trading, and withdrawals occur simultaneously across thousands or millions of accounts. Web3 Compliance must scale to match this operational density.

Risk in exchanges is layered. A single high-risk deposit can spread through internal transfers, trading activity, and secondary withdrawals. Web3 Compliance requires the ability to reconstruct fund paths, identify indirect exposure, and understand how suspicious activity propagates across accounts.

Volume also creates structural pressure. As user activity increases, manual review processes break down. Exchanges need automated risk scoring, prioritized alert queues, and standardized investigation workflows to ensure that high-risk cases are addressed quickly and consistently.

Regulatory expectations further increase complexity. Exchanges often operate across multiple jurisdictions, each with distinct AML and CFT requirements. Web3 Compliance must support adjustable thresholds, region-specific risk logic, and defensible reporting standards without fragmenting internal controls.

For exchanges, compliance is not only about avoiding penalties. It is about maintaining banking access, preserving licenses, and building institutional credibility. In a bid to solve this, Phalcon Compliance embeds scalable monitoring, configurable risk engines, and structured investigation support into exchange infrastructure, allowing Web3 Compliance to function as a core operational layer rather than an external control.

Conclusion

Web3 Compliance is no longer about reacting after something goes wrong. In fast-moving blockchain environments, delayed reviews and manual checks create regulatory risk. A modern compliance framework must detect issues as transactions happen, not weeks later.

At its core, Web3 Compliance transforms AML and CFT requirements into real-time operational controls. Address screening, transaction monitoring, risk scoring, and structured reporting must work together as a continuous system. This allows you to prevent exposure early instead of explaining failures afterward.

Web3 Compliance also replaces fragmented manual workflows with scalable automation. As transaction volume grows, consistent rule enforcement and documented review processes become essential. Regulators and banking partners expect proof, not promises.

Phalcon Compliance supports this shift by embedding compliance logic directly into transaction infrastructure. When Web3 Compliance functions as live financial crime prevention infrastructure, you protect licenses, preserve banking relationships, and build long-term institutional trust.

Frequently Asked Questions About Web3 Compliance

- How is Web3 Compliance different from traditional compliance?

Traditional compliance focuses on centralized financial systems, where banks control customer data and transaction records. Web3 Compliance operates in decentralized environments, where transactions are on-chain and identities are often pseudonymous. This requires stronger blockchain analytics, wallet risk assessment, and continuous transaction monitoring instead of relying only on internal account records.

- What legal standards apply to Web3 Compliance today?

Web3 Compliance is shaped by global AML and CFT regulations. The Financial Action Task Force (FATF) requires virtual asset service providers to follow similar standards as traditional financial institutions. This includes sanctions screening, suspicious activity reporting, and cross-border compliance requirements such as the Travel Rule. Regional regulators also impose additional digital asset obligations.

- What role does KYC play in Web3 Compliance?

KYC helps reduce anonymity risk in regulated Web3 environments. While blockchain addresses do not directly reveal identity, regulated platforms must verify users before providing services. Linking identity verification with on-chain monitoring strengthens AML controls and supports regulatory accountability.

- What tools are commonly used in Web3 AML compliance?

Common tools include wallet address screening, sanctions list matching, real-time transaction monitoring, risk scoring models, cross-chain analytics, alert management systems, and structured reporting workflows. Advanced compliance systems also support fund flow tracing for deeper investigation of suspicious activity.

- What are the biggest challenges in implementing Web3 Compliance?

Major challenges include pseudonymous identities, irreversible transactions, rapid cross-chain fund movement, and constantly evolving regulatory standards. High transaction volumes also create operational pressure. Platforms must balance automation, risk detection accuracy, and defensible reporting processes.

- How can Web3 Compliance scale with institutional adoption?

As digital asset activity grows, compliance systems must scale without losing control. This requires automated monitoring, configurable risk logic, standardized workflows, and clear audit trails. Scalable Web3 Compliance ensures institutions can expand operations while maintaining regulatory trust and banking access.