Starting a crypto payment or OTC trading business in Hong Kong in 2026 requires more than one regulatory conversation. Many founders assume there is a single “crypto license.” That is no longer true.

Hong Kong uses a dual licensing framework. If your business handles fiat currency exchange or remittance, you may need a Money Service Operator (MSO) license. If your business deals in virtual assets or offers OTC brokerage services, you might need a VA OTC license. This is part of a different regulatory system.

These are not interchangeable.

Understanding the difference between MSO and VA OTC is critical. Picking the wrong structure can delay banking access. It can also create regulatory violations or block expansion plans. This guide explains how both licenses work, how they differ, and how to design a compliant structure in 2026.

Understanding these rules is the first step toward strong crypto compliance in Hong Kong.

MSO vs VA OTC: The Main Differences

To make it easy, here is a simple way to look at them:

| Feature | MSO License | VA OTC License |

|---|---|---|

| What it handles | Fiat money (USD, HKD, etc.) | Virtual Assets (BTC, ETH, USDT) |

| Main Task | Remittance and Money Exchange | Spot trading of Crypto |

| Regulator | Customs (C&ED) | Securities and Futures Commission (SFC) |

| Can it do Crypto? | NO | YES |

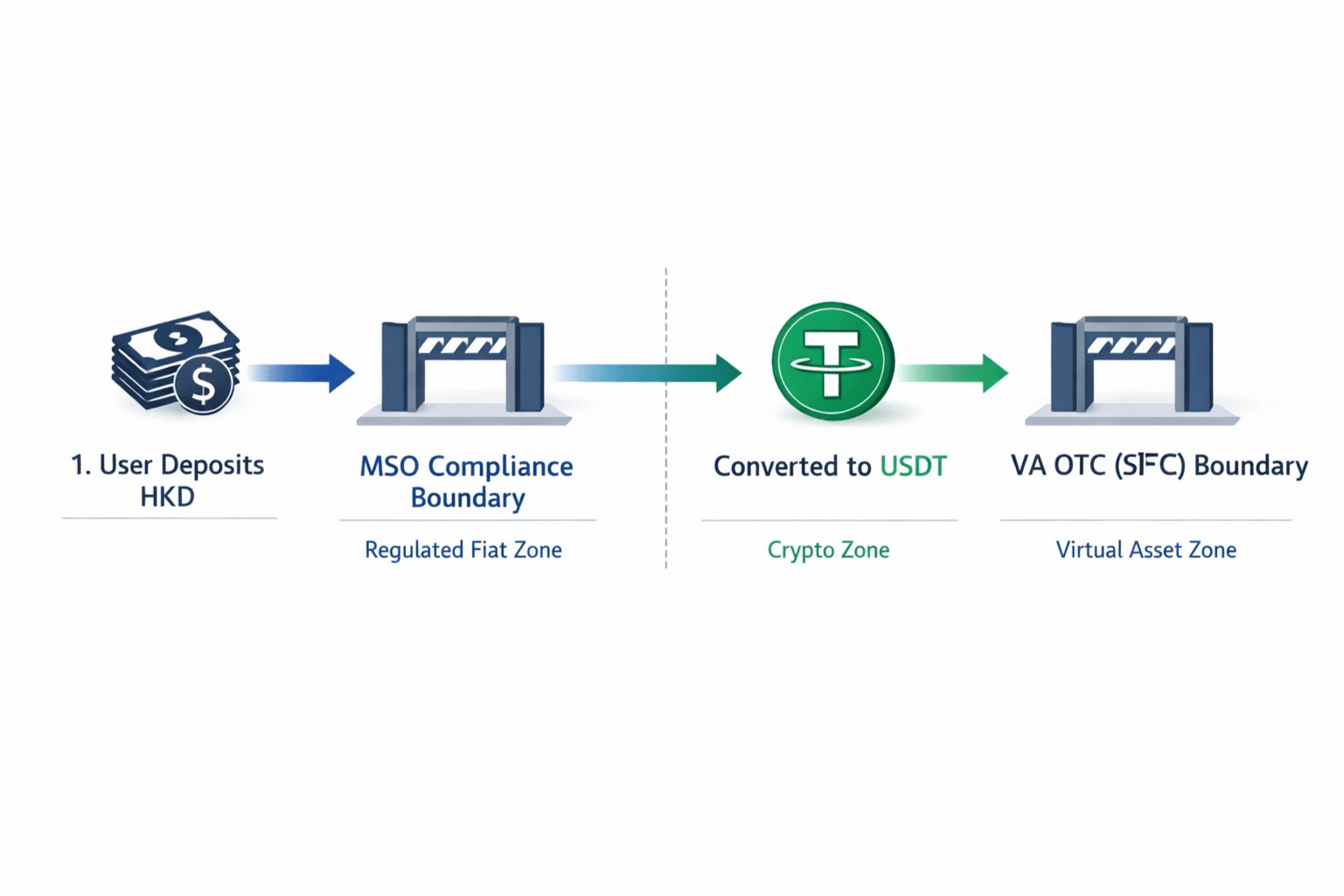

The biggest risk for crypto compliance is "mixing" these two. You cannot use an MSO to do a VA OTC job. If you do, the government will see it as unlicensed trading.

The Hong Kong MSO License

What Is a Hong Kong MSO License?

The Legal Foundation Under AMLO

A Hong Kong MSO license is required for businesses that conduct money changing or remittance activities. It is issued under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO).

This law gives the Hong Kong Customs and Excise Department (C&ED) the authority to supervise money service operators.

The MSO regime focuses only on preventing money laundering and terrorist financing. It does not regulate virtual asset trading.

This is a critical distinction.

The Role of Hong Kong Customs

The Hong Kong Customs and Excise Department regulates MSOs. Customs has long supervised traditional remittance shops and currency exchange businesses.

Crypto companies that handle fiat currency fall under this same framework. But Customs supervises them only for the fiat-related part of their operations.

Customs can conduct inspections. It can request documents. It can suspend or revoke licenses if AML standards are not met.

Important Clarification: What the MSO License Does NOT Cover

The MSO license does not allow a business to trade, broker, or exchange virtual assets.

If an MSO claims it can legally convert USDT to other virtual assets under its MSO license alone, that is incorrect under Hong Kong law.

The MSO license covers:

-

Fiat currency exchange

-

Fiat remittance

-

Cross-border money transfer involving fiat It does not cover:

-

Virtual asset dealing

-

Crypto brokerage

-

Token-to-token trading

Crypto payment firms must separate their fiat operations from their virtual asset activities.

Why the MSO License Still Matters for Crypto Payments

Many founders focus only on virtual asset licensing. But they overlook the fiat side.

If your business processes Hong Kong dollars, US dollars, or other fiat currencies, you may trigger MSO obligations.

Banks expect crypto companies that handle fiat to hold the correct MSO license. But holding an MSO license does not guarantee banking access.

Banks will also examine:

- Your AML program

- Your transaction monitoring system

- Your internal controls

- Your senior management

So, the MSO license is necessary. But it is not enough by itself.

Who Needs a Hong Kong MSO License?

Fiat to Crypto Entry Points

If your platform takes Hong Kong dollars and converts them to crypto, the fiat conversion could follow money changing rules.

But remember: the MSO license only covers the fiat side. The crypto-dealing part may require a separate VA OTC license.

Crypto to Fiat Settlement

If you convert crypto into fiat and transfer funds to a customer’s bank account, the fiat remittance element may trigger MSO requirements.

Again, the virtual asset dealing activity must be assessed separately.

Cross-Border Fiat Transfers

If your business moves fiat money around, like with stablecoin settlements, you may need an MSO license.

The key trigger is fiat movement, not the existence of blockchain technology.

Payment Gateways and OTC Counters

If you operate a physical exchange counter or an online gateway that processes fiat payments, you may require an MSO license.

Even if you outsource parts of the flow, regulators look at substance over form. If you control or facilitate fiat transfers, you may fall within the scope.

How to Apply for a Hong Kong MSO License Step by Step

Step 1 Incorporate a Hong Kong Company

You must first establish a Hong Kong legal entity. Secure a physical office and appoint directors and senior management.

Step 2 Develop Your Compliance Framework

Get your AML policies ready. Also, prepare your risk assessment and internal control procedures, appoint a Compliance Officer (CO) and Money Laundering Reporting Officer (MLRO). Do this before you submit your application. Regulators expect you to be ready before operations begin.

Step 3 Prepare Application Documents

You will need to submit detailed information about:

-

Shareholders and ultimate beneficial owners

-

Directors and senior management

-

Business model and transaction flow

-

Compliance officer details

-

Internal control measures

Audited financial reports or proof of working capital (typically at least HKD 500,000)

Step 4 Submit to Hong Kong Customs

Applicants submit applications to the Hong Kong Customs and Excise Department. Follow-up questions and interviews are common. Transparency and clarity improve approval chances.

Step 5 Post Approval Setup

After approval, ensure your reporting systems and monitoring tools are fully operational. Licensing is the starting line, not the finishing line.

The Hong Kong VA OTC License

What is a VA OTC License?

VA OTC (now broadly categorized as Virtual Asset Dealing) is a newly evolved regulatory regime in Hong Kong. While initial proposals in early 2024 suggested regulating OTC shops through the Customs Department, the final regulatory scheme finalized in mid-2025 saw a major shift. Today, regulatory authority over VA OTC and dealing services is explicitly assigned to the Securities and Futures Commission (SFC).

This shift embodies the principle of "same business, same risks, same regulation." Unlike the MSO, the VA OTC license is all about the virtual assets. It allows you to provide spot trading services, crypto-to-crypto swaps, and stablecoin-to-fiat conversions. In 2026, the SFC uses this framework to strictly oversee crypto brokers, online dealing platforms, and physical OTC shops.

For a crypto payments company, this is the critical second half of the puzzle. If you want to take a customer's fiat cash and convert it into USDT, the MSO alone will not protect you—you must have the SFC-regulated VA OTC (Dealing) license to execute the crypto leg of the transaction. Furthermore, for integrated platforms planning long-term expansion, regulatory guidance increasingly suggests obtaining an SFC Type 1 (dealing in securities) license concurrently. This future-proofs your business in case a token you trade is later re-classified as a security.

Who Needs a Hong Kong VA OTC License?

Stablecoin to Fiat Conversion as a Dealing Service

If your business converts stablecoins to fiat as part of a trading arrangement, you may trigger VA OTC rules. This is common in OTC desks and broker models that handle stablecoin settlements.

But remember: the MSO license only covers the fiat movement. The crypto conversion itself can be virtual asset dealing. So it may need VA OTC licensing.

Crypto to Crypto Swaps Offered to Clients

If you offer token to token conversion for customers, you may be providing a dealing service. This applies even if you call it a “conversion” instead of a “trade.”

This means a business can trigger VA OTC requirements without touching fiat.

OTC Brokerage and Trade Matching

If you introduce buyers and sellers and earn a fee, you may be acting as a broker. This is a classic VA OTC use case.

It does not matter if you match trades through a website, a chat group, or a private network. What matters is the business activity.

Block Trades for Institutions and High Net Worth Clients

If you offer large size trades that are not publicly quoted, you may fall within VA OTC scope. This includes customized pricing, negotiated settlement terms, and private execution.

These services are often the core of institutional OTC models.

Physical OTC Stores and Online OTC Platforms

If you run an OTC shop or an online OTC desk that buys or sells virtual assets, you may need a VA OTC license.

The channel does not change the licensing trigger. A storefront and an online desk can be treated the same if they perform the same dealing function.

Why Crypto Payment Companies Often Need Both

If you are building a crypto payments app in Hong Kong, you are likely doing two things:

- Moving fiat money for users (Remittance).

- Swapping that fiat for crypto (Trading).

This means you might need both licenses. One handles the "money" side, and the other handles the "crypto" side.

In 2026, regulators want to see a clear line between these two. You must show where the cash stops and where the crypto starts. This is the heart of crypto compliance. If you try to hide crypto trades inside an MSO business, you will get flagged very fast.

How Phalcon Compliance Supports Hong Kong MSO and VA OTC Businesses

Operating under a dual licensing framework is legally safe, but it is operationally complex. You have to satisfy two different regulators—Customs (C&ED) for your fiat flows and the SFC for your virtual asset flows.

Many payment companies fail because their compliance tools cannot bridge this gap. Traditional banking AML tools can’t read blockchains. Also, basic crypto tools don’t grasp regulatory reporting. In 2026, SFC inspectors and conservative Hong Kong banks demand real-time proof that your funds are clean.

This is where Phalcon Compliance becomes the backbone of your operations. Here is how it specifically supports Hong Kong crypto payment firms:

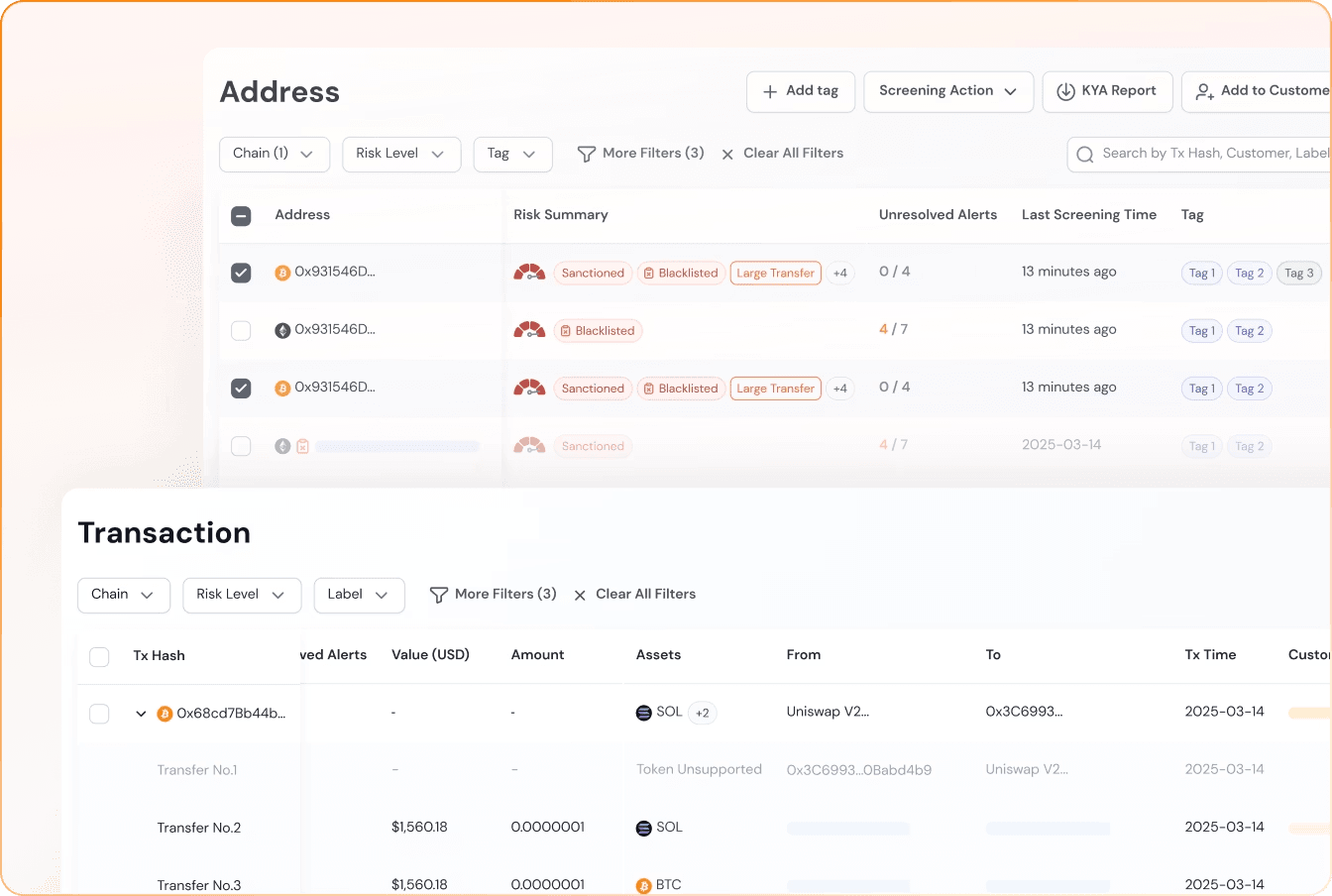

1. Real-Time KYT (Know Your Transaction) for SFC Standards

The SFC asks VA OTC licensees to use strong risk management.

Phalcon Compliance analyzes incoming and outgoing crypto transactions before they settle. By using an advanced automated KYT (Know Your Transaction) engine, it checks the history of wallet addresses to ensure funds are not linked to darknet markets, hacks, or sanctioned entities. Block high-risk crypto deposits right away. This keeps your fiat business safe from contamination.

2. Multi-Chain Visibility for Stablecoin Settlement

Crypto payment companies rely heavily on stablecoins like USDT and USDC. These assets move across multiple chains (Ethereum, Tron, Polygon, etc.). Phalcon tracks risk natively across all major blockchains. If a user tries to obscure funds by "chain-hopping" before depositing to your OTC desk, Phalcon uncovers the complete risk path.

3. Clear Boundary Management for Dual Licenses

To satisfy both Customs and the SFC, you must prove where fiat stops and crypto begins. Phalcon provides detailed, auditable records for every digital asset transaction. When Hong Kong banks audit your MSO business, you can create structured reports. These reports show how you manage crypto risks. This helps build your banking partners' confidence in keeping your fiat accounts open.

Final Thoughts: Master the Dual-Track System

In 2026, the days of running a crypto payment business in Hong Kong with a single, vague license are completely over. The regulatory landscape has matured into a sophisticated, dual-track system.

If your business touches fiat currency, you must respect the Customs Department and secure an MSO license. If your business facilitates the conversion or trading of digital assets, you must answer to the SFC under the VA OTC dealing regime. Hiding crypto operations with an MSO license is a quick way to spark enforcement actions and lose your banking partners.

The most successful Web3 payment gateways and OTC desks in Hong Kong do not fight this complexity—they build around it. To turn regulation into a competitive advantage, understand the roles of the C&ED and SFC. Next, acquire the right licenses, including SFC Type 1 uplifts. Then, use advanced tools like Phalcon Compliance for real-time monitoring.

Licensing gets you into the Hong Kong market. Flawless, automated compliance is what allows you to stay.

Frequently Asked Questions (FAQ)

- Can a foreign company apply for a Hong Kong MSO or VA OTC license?

Yes, foreign companies can apply. You must either set up a local Hong Kong company or register your foreign company as a non-Hong Kong company with the Companies Registry. Both C&ED and the SFC need real local "substance." This means you must have a physical office in Hong Kong and local senior management or compliance officers.

- How much capital is required to get a VA OTC license in Hong Kong?

The paid-up capital requirements can change based on whether you have an SFC Type 1 license or just act as a dealer. The SFC expects crypto businesses to hold enough liquid capital. This helps them manage operational risks. For VA-related activities, the costs often reach millions of HKD. This is a big increase from the low capital needs of a traditional MSO.

- Does an MSO license allow me to issue my own stablecoin?

No. In Hong Kong, issuing a fiat-referenced stablecoin (FRS) is regulated by a unique framework. This framework is managed by the Hong Kong Monetary Authority (HKMA). The MSO license only allows the remittance and exchange of fiat money. In contrast, the VA OTC license covers the trading of stablecoins.

- What are the penalties for operating an OTC crypto desk without a license?

Operating an unlicensed money service (MSO) or virtual asset dealing business in Hong Kong is a serious criminal offense. Penalties can be severe. They include shutting down the business immediately. Fines can be hefty, sometimes over $1,000,000 HKD for VA offenses. Directors and senior management may also face prison time.

- Can I use a personal bank account to run my MSO or VA OTC business?

No, you can't. Hong Kong banks have a strict zero-tolerance policy. They do not allow personal accounts for business purposes. This rule is especially true for MSBs and crypto trading. You must secure a corporate bank account. Banks will open these accounts only after checking your AML/KYT systems. They also need to verify your corporate licenses.

- How long does the application process take for these licenses?

An MSO license typically takes 3 to 6 months to process once a complete application is submitted to Customs. SFC-regulated licenses, such as VA OTC / Type 1, are much stricter. They can take 9 to 18 months to get. The time frame depends on a few factors: the complexity of your business model, the readiness of your compliance tech (like your KYT systems), and how quickly you respond to SFC queries.

- Why do some crypto platforms also apply for an SFC Type 1 license?

The regulatory status of tokens can change. A token considered a "utility" today might be reclassified as a "security" tomorrow. Getting a Type 1 (Dealing in Securities) license with the VA Dealing license helps crypto platforms. This protects their business and allows them to trade more digital assets. They can do this without any interruptions.