In plain language, money laundering is the process of taking money that came from something illegal and making it look like it came from a normal, legal source. That is the whole idea in one sentence.

The name itself comes from the early 1900s, when criminals ran cash through laundromats. A laundromat was a cash-heavy business where dirty money could be mixed with legitimate revenue and reported as income.

The mechanics are different today. The core idea is the same: take money that came from something illegal, and make it look like it came from something legal.

The sections below explain how it works in plain language (no jargon, no assumed knowledge) and show why crypto has made the problem significantly harder to stop.

Money Laundering, Explained Like You're New to Finance

Imagine a drug dealer with $100,000 in cash. That cash is dirty. If they try to buy a car, open a bank account, or pay taxes with it, investigators might ask where it came from. They cannot explain it without admitting to a crime.

Money laundering solves that problem. The goal is to run the money through a series of transactions until it looks like it came from a normal business. At the end, the criminal can spend it, invest it, or deposit it. They can do all of this without raising suspicion.

Cornell Law School defines money laundering as the process of taking money obtained from criminal activity and making it appear legitimate. The definition is simple. The methods used to accomplish it are not.

Three words you'll see in any AML (Anti-Money Laundering) discussion:

-

Placement: getting the dirty money into the financial system for the first time

-

Layering: moving it around to make the trail confusing

-

Integration: spending or investing the money like it is normal income

Think of it like this. Placement is hiding cash under a mattress and then sneaking it into a bank account slowly. Layering is moving that money between five different accounts in three different countries. Integration is buying a house with the result and calling it savings.

Why Criminals Love Crypto

Crypto makes money laundering easier for specific reasons, but it is not impossible to trace.

In the old days, criminals used physical cash, shell companies, and offshore bank accounts. Those methods are slow. They require lawyers, accountants, and complicit banks. They leave paper trails.

Crypto is faster. Moving $1 million in Bitcoin takes seconds. It does not require a bank account. It works across any border. And while every transaction is recorded on a public ledger, reading that ledger requires specialized tools that most platforms do not have.

Two 2025 cases show how large the problem has become.

In 2025, U.S. authorities seized $15 billion in Bitcoin from a scam network, the largest seizure in history. To picture that scale, $15 billion is roughly the annual budget of a mid-size U.S. federal agency. The network had tricked victims online, then laundered the money through crypto exchanges (BlockSec analysis of the 2025 $15B Bitcoin seizure).

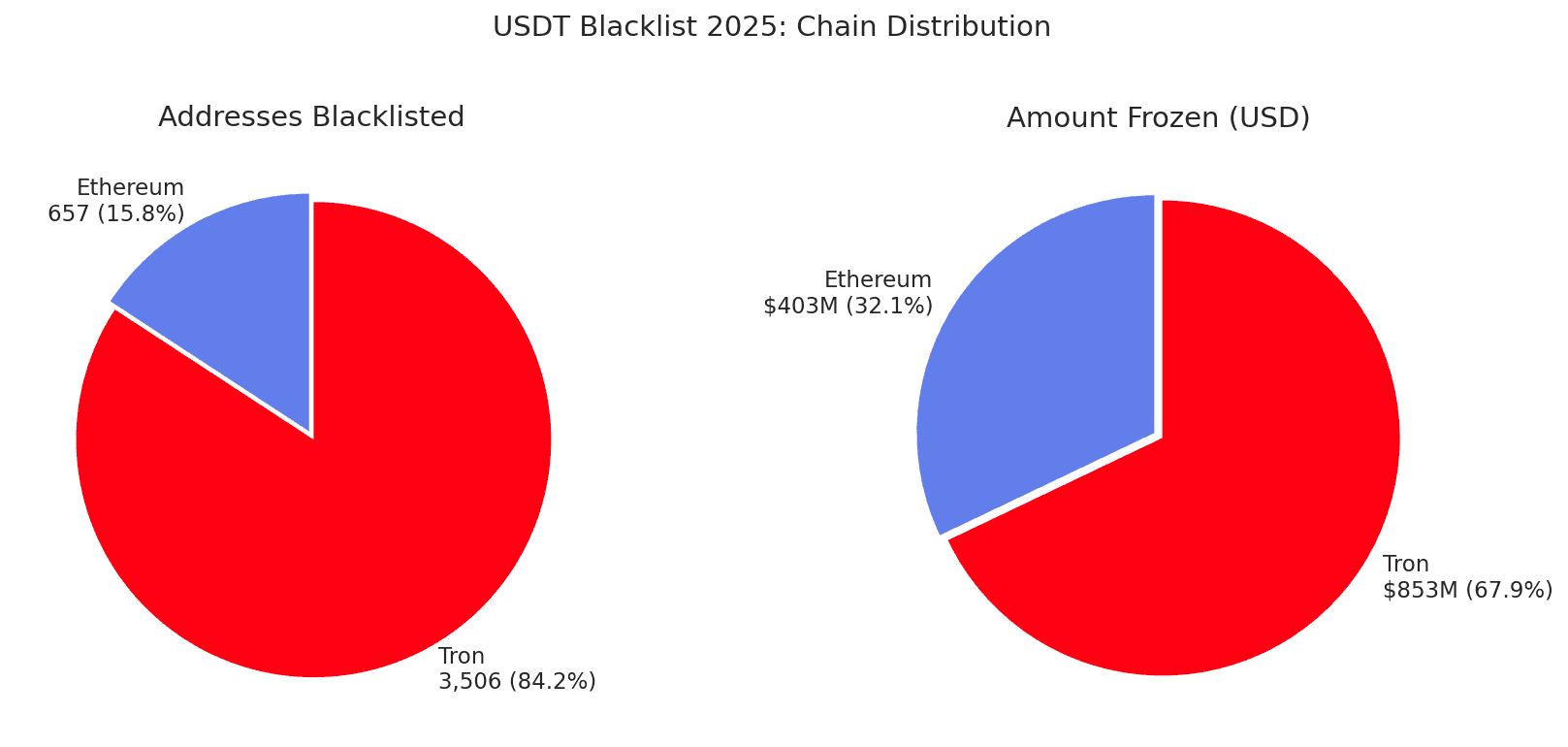

In 2025, Tether froze $1.26 billion in suspicious USDT funds across 4,163 addresses. That is enough to fund a small country's national budget for a year. BlockSec's analysis of $1.26 billion in USDT frozen in 2025 found that 96.4% of that money was never returned, meaning less than 4% was ever unfrozen.

Those numbers show the scale. Authorities seized $15 billion and froze $1.26 billion. Crypto money laundering is not a niche problem. It is operating at scale that matches or exceeds traditional financial crime.

The Three Stages in Plain Language: Placement, Layering, and Integration

Here is a plain-language breakdown of the three stages, including how they map to crypto.

| Stage | Plain Language | How Crypto Is Used | Why It's Hard to Catch |

|---|---|---|---|

| Placement | Getting dirty money into the system | Converting cash or fraud proceeds into USDT or Bitcoin | Peer-to-peer exchanges, unhosted wallets, no bank account needed |

| Layering | Making the trail confusing | Moving funds across multiple wallets, chains, and exchanges | Dozens of hops in minutes; cross-border with no correspondent bank involved |

| Integration | Spending the money like it's normal | Withdrawing to a centralized exchange, converting to fiat, buying assets | Funds look identical to legitimate crypto transactions at this point |

For a more technical breakdown of how each stage works in crypto, see our explainer on What Is Money Laundering.

The United Nations Office on Drugs and Crime estimates that 2–5% of global GDP is laundered every year (a widely cited UNODC estimate). That is between $800 billion and $2 trillion. In crypto, the laundering happens faster than in traditional finance, but it also leaves a permanent record on the blockchain.

That permanent record is the basis for modern AML tools. The challenge is building tools that can read millions of transactions fast enough to catch laundering before it completes.

Two Free Tools Anyone Can Use to Check

You do not need to be a compliance professional to look up whether a crypto address has a risky history.

MetaSleuth is a free blockchain investigation tool. Enter a wallet address and MetaSleuth shows you where the funds came from and where they went. It also shows whether the address is connected to anything flagged as suspicious across 13 blockchains on a single screen. It is the same tool used by law enforcement agencies and compliance teams.

USDT Freeze Checker is a free tool built by BlockSec. If you want to know whether a specific USDT address has been frozen by Tether (on either Ethereum or Tron), paste the address and get an instant answer. No account required.

Both tools are useful for individuals who want to check an address before sending funds, and for small platforms that want a quick first-pass check before a more comprehensive compliance review.

Implications for Personal and Platform Crypto Users

If you use crypto personally, the key takeaway is this: on-chain records are permanent. If an address you transacted with is later flagged as connected to money laundering, that connection is visible in the transaction history. Checking the source of funds before accepting a large crypto transfer is not paranoia. It is basic protection.

If you run a crypto platform (an exchange, a DeFi protocol, or a payment service), the stakes are higher. Global compliance standards are tightening, according to the FATF Virtual Assets 2025 Update. Platforms that cannot demonstrate AML screening are facing increased regulatory pressure across every major jurisdiction.

The simple terms version of crypto compliance is this: check addresses before you let them transact on your platform. If a wallet has moved funds through a known scam network, a mixer, or a frozen USDT address, that is visible on-chain. The tools to see it exist.

Want to see whether a crypto address has ever been flagged? Try MetaSleuth. It's free.

If you run or build on a crypto platform, for how AML compliance works in practice for exchanges and VASPs, see AML Compliance for Crypto.

Frequently Asked Questions

Q: Are small personal crypto transfers (amounts under $1,000) monitored for AML purposes?

Yes. Compliance platforms look at the wallet's history, not just the amount. A $200 transfer from a wallet linked to a scam or a sanctioned address will be flagged on most major exchanges, even though it is small. Separately, FinCEN's Travel Rule requires registered money services businesses to share information on transfers of $3,000 or more. The two checks work side by side: one looks at the wallet, the other at the transfer size.

Q: Do crypto exchanges proactively report suspicious users to regulators, or only respond to subpoenas?

Both. U.S. exchanges are required to file a Suspicious Activity Report (SAR) on their own when they spot something off, they do not wait for a subpoena. The trigger is $5,000 in suspicious activity. Major exchanges like Coinbase and Kraken publish transparency reports showing how many SARs they file. When an exchange skips this duty, the penalties are steep: in 2023, Binance settled with FinCEN after failing to file required SARs for years.

Q: Are stablecoins easier for regulators to freeze than other cryptocurrencies like Bitcoin or Ether?

Yes, much easier. USDT and USDC are run by companies (Tether and Circle) that can switch off a specific wallet from the inside. Bitcoin and Ether have no company in charge, so the only way to freeze them is to seize the wallet's private keys, which usually takes a law enforcement operation. That is why Tether was able to freeze $1.26 billion across 4,163 addresses in 2025, something that would be almost impossible to do directly on Bitcoin.

If you run a crypto platform, → book a Phalcon Compliance demo and see how automated AML screening fits your workflow — Book a demo